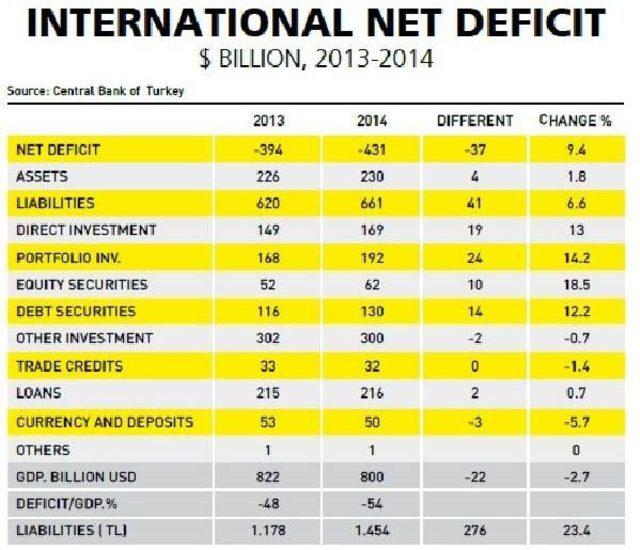

- Turkey’s foreign liabilities have jumped by $41 billion while the rise in its foreign assets remained at $4 billion, revealing the vulnerabilities of the country.

The “equilibrium” situation in countries’ relations with global economy has vital significance. How much a country can cover its foreign debts to global markets and other liabilities with its assets it has contributed to the global economy, in other words, with its investments in the external world and with its domestic gold and foreign currency reserves? If there is a gap in its liabilities versus assets, what is its dimension and where does this stand at its national income?

This indicator and similar ones, reveal the fragility coefficient of countries. The method to measure this has been determined by the IMF and it collects information from member countries with a handbook.

How much are your assets, how much are your liabilities and thus what is the dimension of your gap or surplus?

In Turkey, the Central Bank produces the International Investment Position (IIP), which is the stock value at a certain date of external financial receivables and financial assets versus external financial liabilities. This statistical data is updated every month.

In IIP, the difference between the total financial assets and total financial liabilities, is named the net international investment position. In other words, the net international investment position is the net of Turkey’s receivables from other countries and Turkey’s debts to other countries. The IIP can be negative or positive.

For Turkey and similar countries, the IIP is generally negative. External assets are not enough to meet external liabilities. This situation changes from year to year. The rate of Turkey’s assets meeting its liabilities and the size of its external gap according to its national income are increasing instead of decreasing every year and its risk coefficient is rising.

The picture at the end of 2014

Last week, Turkey’s IIP gap was declared for 2014 as $431 billion by the Central Bank. In the Central Bank data for December 2014, while Turkey’s external asset-receivable amount was defined as $230 billion, the amount of its external debts and other liabilities were reported to have reached $661 billion. In this case, as of the end of 2014, Turkey’s position gap has reached $431 billion and it has surpassed the gap of 2013 by $37 billion.

This means only 35 percent of meeting debts and liabilities and that Turkey has a disadvantage of 65 percent. In the wide sense, external debts are 187 percent more than external receivables.

Turkey’s national income of 2014 will be announced at the end of March and it is estimated to be $800 billion. In this case, debts will reach 54 percent of the national income. This rate was 48 percent in 2013. This means the position gap has worsened $37 billion in one year, increasing 6 points.

Beware the course

While Turkey’s external assets increased only $4 billion in 2014, its external debts and other liabilities increased $41 billion. It looks like the value of foreign direct investments in Turkey has increased $19 billion. While the value of foreigners’ investments in securities has been $10 billion, their investments in state bonds increased 14 billion. There was a $2 billion decrease in foreigners’ external debts.

The picture does not look good as of 2014, with $661 billion liabilities versus assets that can only cover nearly 35 percent of them. The fact that assets can only meet 35 percent of liabilities means that there are no assets to cover almost two-thirds of debts and other liabilities. The size of the gap that reaches 54 percent of the country’s national income is considered a significant fragility.

The situation that has emerged at the end of 2014 is the product of a buildup of years. In the first year of the rule of the Justice and Development Party (AKP), which was 2003, Turkey’s assets reached $74 billion while its liabilities were $179 billion. In other words, assets were able to cover 41 percent of the gap that was 35 percent of Turkey’s national income. The year 2003 was one when the AKP prepared to further integrate with global economy and, from there, draw more loans, hot money and direct investments. In following years, warming and integration accelerated.

For more privatizations and purchases, more foreign capital flew in, more hot money went into the stock exchange and state bonds and more loans from foreign banks started to flow in. As a result, debts and other liabilities increased more than the buildup of assets and at the end of 12 years, in other words, in 2014, the rate of the assets meeting liabilities went quite below what it was in 2003, from 41 percent to 35 percent. The amount of foreign gap, in the same period, went up from $105 billion to $431 billion. The rate of the gap in national income hiked to 55 percent from 35 percent.

Among the fragile

The dimensions Turkey’s position gap have reached, even if only Europe is analyzed, show that it is among the leading of the fragile countries. For the IMF, if the rate of the position gap to the national income exceeds about 40 percent, then it is considered that the red line has been crossed. The place Turkey has reached is 54 percent. This is very fragile and it is a rate that would scare foreign investors.

The burden in terms of Turkish Liras

While the average dollar exchange rate was 1.90 Turkish Liras in 2013, the average dollar exchange rate became 2.20 liras in 2014. Thus the increase in the dollar exchange rate reached 16 percent. Both with the effect of the increase in the exchange rate and also the increase in the debts to foreigners, Turkey’s external liabilities increased in terms of liras nearly 24 percent in one year. Its debts and other liabilities in liras increased 276 billion liras to reach 1 trillion 454 billion liras.

In other words, the increasing foreign dependency has giant costs in difference in exchange rates and only in 2014 this exchange rate burden was 276 billion liras and with the dollar exchange rate of 2014, it was $125 billion.

One does not even want to think of the extra burden that would be brought on the position gap with the likely leap in the dollar exchange rate with the U.S.’ interest rate increase.

(GRAPH)

Anadolu Ajansı ve İHA tarafından yayınlanan yurt haberleri Mynet.com editörlerinin hiçbir müdahalesi olmadan, sözkonusu ajansların yayınladığı şekliyle mynet sayfalarında yer almaktadır. Yazım hatası, hatalı bilgi ve örtülü reklam yer alan haberlerin hukuki muhatabı, haberi servis eden ajanslardır. Haberle ilgili şikayetleriniz için bize ulaşabilirsiniz

Haber Gönder

Haber Gönder